Great Divergence or Financialized recovery ?

The IMF’s latest delivery of the World Economic outlook contains an interesting analysis of the current “non” recovery in terms of a divergence between fiscal and monetary policy, the first between restrictive and procyclical in nature and the second being accommodating and reinforcing a financial expansion. As argued here by the IMF economists who worked on this issue, the “great” divergence then is between a stagnating productive economy punished by austerity and a booming financial economy supported by quantitative easing and real low interest rates ? I’ve read here and there analysis of the divergence by a number of commentators, the latest and most interesting being this column by Gavin Davies in the FT,

and I’m wondering if this is what a “Financialized recovery” looks like.

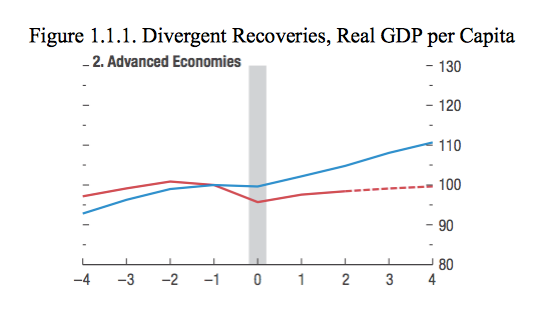

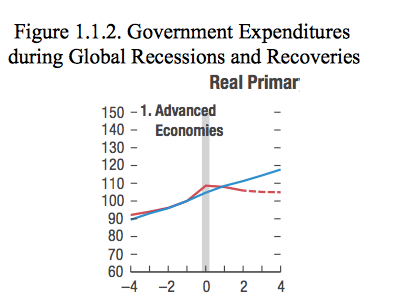

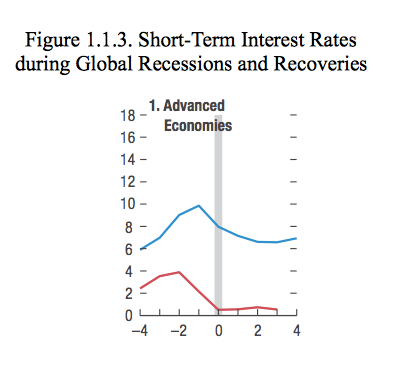

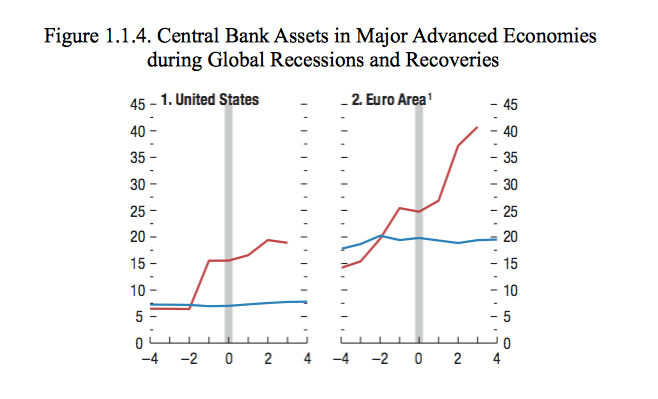

I’ll be udpdating this post later with data on Canada, in the mean time here are 4 charts taken from the WEO report, basically each graph is illustrates comparative data contrasting the current recession/recovery with average outcomes of the 1975, 1981, 1991 recession recovery. The first charts real GDP growth, the second public expenditure, the third interest rates and the last central bank assets. Â For Canada I think that CHMC assets should be used as a complement to data on the BOC’s assets.

The data is organized as follows:

Years from global recession on x-axis; indices = 100 in the year before the global recession. Recovery from the Great Recession in red, Â Average of previous recessions (1975, 1982, 1991) in blue.

You tiff images aren’t being displayed by my version of Firefox.

Re: “the “great†divergence then is between a stagnating productive economy punished by austerity and a booming financial economy supported by quantitative easing and real low interest rates”

See Michael Hudson, The Bubble and Beyond:

http://www.federalreserve.gov/boardDocs/speeches/2002/20021121/default.htm

This summary of my economic theory traces how industrial capitalism has turned into finance capitalism. The finance, insurance and real estate (FIRE) sector has emerged to create “balance sheet wealth†not by new tangible investment and employment, but financially in the form of debt leveraging and rent-extraction. This rentier overhead is overpowering the economy’s ability to produce a large enough surplus to carry its debts. As in a radioactive decay process, we are passing through a short-lived and unstable phase of “casino capitalism,†which now threatens to settle into leaden austerity and debt deflation.

A couple points with regard to a couple intersections in my research right now. First off is the varieties of capitalism and how they have evolved over this period. In a Marxian glean of the circuits of capitalism, one must not overlook his warning of how critical it is to keep money and finance capital within the circuitry and maintaining investment Into productive capital, whether it be In terms of updating the means of production in technology, organizational form and replacement rates. Also the changing skillset and knowledge requirements of labour, through education, training etc. Both of which are through appropriate levels of A mix of public and private investment. The key is levels of investment in productive capital. so the question is, where has productive investment been through the last 3 recessions and more importantly the last 15 or so years?

So now onto my second focus of my research and this with the nature of what has transpired within China in the last 20 years. It is just sheer gargantuan the mount of productive capital I t terms of means of production that has been

invested into china. It is not just the labour that was the attraction, the special economic zones around the pearl river delta at equivalent to the manufacturing capacity of at least the EU. And a majority of it was export based. I am still early I to this research but the level of economic development and the standard of living rise in china is severely discounted in mainstream economics of the west.

So my thesis, a good portion of the investment within many developing countries has been of the wrong variety and hence has caused increasingly stagnant and declining economic outcomes for consumption. That is, investment focused on first financialization of the economy and second and potentially not talked about enough, the merchantilist portion of capital, I.e. retail and wholesale trade, marketing, merchandising and the whole commercial space. It is no coincidence that commercialized capitalists has usurped the commanding heights of a majority of productive capitalists, I.e. the wal marts, the ideas, Nike, Dell, etc.

I would call this the rejection of the fit planet mentality. I am not arguing against globalization, however I am pointing a finger at the distributional aspects of Capital and the motors of change. Do we really have a regional global economy? Just look at some basic statistics on growth and trade flows over the past 20 years and you would have to say no, domestic economies within the regional trade zones and the investment patterns of productive capital I am sure would warrant another look. A couple of examples, steel consumption, and production in the world economy, China was at one point over half the world consumption, and the same holds in several other areas of consumption and production.

The question that gets back to me, given that consumption is mainly driven by consumers, and those consumers are part of an increasingly globalism under several varieties of capitalism, where do we go when financialization of the economy is a spent force, I.e. housing bubbles have proved unstable and a poor surrogate to waged income. Do we now start raising wages of the commercialized sectors of the economy in west? Or will there be a retrenchment of productive capital back to the more developed economies? I am not sure more developed is actually a solid footing anymore, after my month studying china, albeit from a distance and it is a massively complicated economy. However, capitalism has been a runaway succes, if you count merely production GDP statistics. On some other fronts, like wealth polarization, pollution, And a few others, not sure about the outcomes or the longevity. But there are some massive productive economic engines that have been built in

China.

Sorry for going on nd hijacking your post a bit, but it was on my mind.

A couple of typos above, that should be good portion of investment within more developed economies has been financial and commercialized, a big hole in that productive investment space.

Also, many economists paint the regional model of globalization, my point is we have that, but I think the degree and mix of investment has not been regional balanced.

Just wanted to apologize for the massive typos above, my iPad was autocorrecting, and I could not find my glasses which I just started wearing for reading.

Also, I know this stuff is not news to many, but for me it is the dimensions of how far we have let the various forms of capital to flow in a manner that seems quite destructive. Cycle through the circuitry of these flows and it keeps coming back to declining demand that i would argue is the missing component, yet to politically assess the solution space being put forward in any trading zone be it the EU with its austerity and structural adjustments medicine for the southern countries, to Asia with China slowing after such a massive expansion, not sure how they were expected to keep that pace, to Japan and its lost decade, and the taming of the Asian tigers, to north America with its financialized, too big to fail but busted housing market and the push to austerity and anti worker pro business low tax policy- no where do we see consumption get it due mention. Check that, France announced today it might start thinking about it, and Spain may pull back some austerity targets.

Anyway, so much talk in the policy circles but none that seem to focus on the addressing the problem.

Pt

http://www.nakedcapitalism.com/2013/06/chinas-minsky-moment.html

Was reading the above article and I recalled Eric’s post here and how it still sits deeply in my living space. Seems like one of the largest economies of the world is increasingly being drawn to the dark side of financialization- at least that is what the author seems to be building an argument towards. However, it could be, that as China strives towards expanding its consumer based economy, lending rates and credit would expand, similar to a western actually existing growth strategy- that is makes sure consumers have lots of credit and do not worry about the wages. There has been wage growth in China, but the question is, are we experiencing a short gasp of breath after such immense growth? Or will there be a failure to create internal consumer growth? Some say the super growth will continue for at least another 10-15 years. Others, well, they look at internal tensions, a lack of labour market wage pressures (however- that is not to say markets are totally in charge here), a declining global demand, and a increasing competitiveness. Personally, my feeling, concludes a mix of both, a very unsteady move towards rural migration into the cities seems a bit dampened but not a spent force- the polarization in both qualitative and quantitative living standards will keep the semi- migration (what a mess these workers live in long periods away from their rural homes living in dorms and such) and permanent migration going – extensive polarization will keep the power brokers worried about destabilization- and I do not believe the notion that authoritarians do not fear the masses- they do- 5000 years of history speaks volumes. There have been some massive gains in living standards- the question is how far and diffused with this distribution of wealth unfold- lot of road blocks.