The R Word

That sinking feeling is coming on. The US economy is slowing and several well-respected economists have made their call. Leading off, Paul Krugman:

The key point is that the forces that caused a recession five years ago never went away. Business spending hasn’t really recovered from the slump it went into after the technology bubble burst… Also, the trade deficit has doubled since 2000, diverting a lot of demand away from goods produced in the United States.

Nonetheless, the economy grew fairly fast over the last three years, mainly thanks to a gigantic housing boom. This boom led directly to unprecedented spending on home construction. It also allowed consumers to convert rising home values into cash … so that … spending could run far ahead of … incomes…

Even optimists generally concede that the housing boom must eventually end… But the conventional wisdom was that housing would have a “soft landing  You might say that the theory was that business investment and exports would stand up as housing stood down.

The latest numbers suggest, however, that this theory isn’t working much better on the economic front than it is in Baghdad. … Now, for the first time, problems in the housing market are starting to seriously reduce economic growth: the latest … data show real residential investment falling at an accelerating pace…, falling employment in home construction, and [falling] retail employment … suggesting that consumer spending is running out of steam. (Gas at $3 a gallon doesn’t help…) …

Now maybe we’ll still manage that soft landing despite a rapidly rising number of unsold houses; or maybe there’s a boom in business investment and/or exports just over the horizon. But based on what we know now, there’s an economic slowdown coming.

This slowdown might not be sharp enough to be formally declared a recession. But weak growth feels like a recession to most people; remember the long “jobless recovery†that followed the official end of the 2001 recession?

And what will policy makers do about a slump, if it happens? A snarky but accurate description of monetary policy over the past five years is that the Federal Reserve successfully replaced the technology bubble with a housing bubble. But where will the Fed find another bubble?

Next up is Brad DeLong:

As of the beginning of August 2006, a recession is not here, and I’m not going to violate my own rule by saying one is coming. But there is a good chance — for the first time since 2003 — that there might be a recession in progress six months from now.

Why?

Three factors: 1) A Federal Reserve that finds itself with less inflation-fighting credibility than it thought it had; 2) upward pressure on inflation from rising energy and, perhaps, import prices; and 3) millions of middle-class homeowners who for too long have treated their houses as gigantic ATMs, using home equity loans and refinancing to generate extra spending money.

…

Make no mistake about it: The U.S. economy is close to the edge. Retail sales in the second quarter were rising at only a 2.1 percent annual pace. Business investment in equipment and software was falling. Residential construction was falling. Either households will continue spending beyond all reason, or businesses will start boosting investment, or exports will start booming, or there will be a recession sometime in the next year. Figure the odds at 3 out of 10.

What can be done to head off the danger? Unfortunately, very little. The bag of macroeconomic tricks is empty. In 2000-2001 the Federal Reserve could lower interest rates to the floor, boosting residential construction and consumer spending to offset the decline in high-tech investment, and turn the 2001 recession into a very small event indeed. In 2002-2003 the short-run stimulative effect of the Bush tax cuts came online at exactly the right moment to offset fears of a deflationary spiral. But today further fiscal stimulus would increase global imbalances — meaning, raise the trade deficit — and do more damage to confidence than it might do good in curing a recession. And sharp reductions in interest rates would lower the value of the dollar and increase inflationary pressures from import prices in a way that the Federal Reserve does not dare allow.

Nouriel Roubini has upped his probability of a US recession in 2007 to 70% up from 50% just last week. He writes:

I have reviewed in my latest writings the flow of macro indicators for the U.S. economy… these indicators suggest that the Three Ugly Bears that I warned of since last fall are becoming uglier by the day: the housing slump is becoming a real bust; oil is headed higher and higher…; and inflation – both core and headline – is rising further forcing policy makers across the world to increase interest rates. Housing alone is now enough to cause a severe U.S. recession…

On top of the housing bust, the rising oil prices are adding another severe stagflationary shock to the economy. And the interest rate increases “in the pipeline” (to use the Bernanke term) still have to negatively affect the economy as the economy today is reacting – given the long lags of monetary policy – to the effects of a Fed Funds at 4%, not the current 5.25% whose effects will be felt only in 6-9 months.

…

markets, investors and policy makers will soon wake up from the delusional dreams and the fairy tales they have been indulging into for too long and will face the five ugly realities that I described above:

1) the U.S. will experience a sharp slowdown followed by a severe recession;

2) the Fed will pause and then ease in the fall but such easing will not be able to prevent the U.S. recession;

3) after a suckers’ rally following the Fed pauses and easing, stock markets will enter into a bearish contraction phase; and other risk assets will also experience sharp drops. In 2006, cash is king;

4) the rest of the world will not decouple from the U.S. recession and there will be no “rotation†in global growth as the rest of the world will sharply slow down – after a short lag – following the U.S. recessionary lead;

5) the risk of a disorderly rebalancing of the growing global current account imbalances is increasing with serious consequences for the U.S. dollar and with the growing risk of dangerous global trade and asset protectionism.

Then, in this most volatile and dangerous macroeconomic, financial and geopolitical situation, the risk of a US recession turning into a systemic financial meltdown cannot be ruled out. There are serious similarities between the situation today and the forces that led to the stock market crash – 20% in one day – in October 1987.

Finally, here is Robert Reich, responding to weak employment numbers:

What’s happening? Mainly, a slowing economy that’s particularly affecting home construction, where a significant portion of job growth in the last few years had been coming from. What’s the significance? More people out of work, typically for a longer period of time. More importantly, lots and lots more people who know someone who’s lost a job or can’t find one, news that sends a chill into the wallets and pocketbooks even of those who have jobs. Which, in turn, means a lower rate of buying. Which, in turn, further slows the economy. Add in higher fuel prices for the typical family (gas, air conditioning, etc) and we’re facing increasing odds of a r** (a word not to be written unless the odds become so high that the mere mention does not contribute to its arrival). But be warned nontheless.

Yikes! My spidey senses have been tuned to this recession meme all year, largely on the basis of the housing market, interest rate increases, and those unresolved global macro imbalances that could be the biggest danger of all.

What does this mean for Canada? After all, the US went into recession in 2001, while Canada had a slowdown but did not drop into negative territory. On the other hand in the early 1990s, the mix of higher Bank of Canada interest rates due to John Crow’s determination to wipe out inflation plus the structural adjustments from the Canada-US free trade agreement led to a deeper and longer recession in Canada.

A few days ago, Statistics Canada released its May update for the national accounts, which show flattening of real GDP growth despite the record low unemployment rates seen over the past year:

Economic activity remained essentially unchanged in May, edging up 0.1% in both March and April. Goods production declined (-0.5% in May) for a third straight month, more than offsetting the gain in services (+0.2%). Except for a slight advance in the manufacturing sector, the main goods producing sectors (mining, oil and gas extraction and construction) declined in May. For services, the largest gains were registered in wholesale trade, the financial sector and public administration. Retail trade was down.

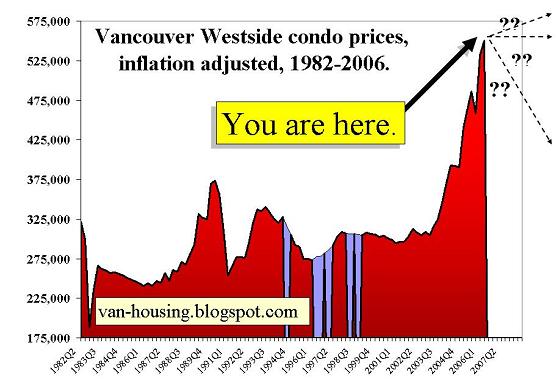

The outcome of all this probably depends on where you live, though we have no provincial GDP numbers right now. Continued high oil and gas prices, and high energy prices in general, will be good for Western Canada and the new petro-provinces of Newfoundland and Nova Scotia. In BC, other commodity prices for lumber and minerals may also offset the downward trend. And in Vancouver, where I live, Olympic Keynesianism may save our bacon to some extent, although the excesses of the housing market seem particularly acute here (see this figure, courtesy of the Vancouver Housing Market Blog). In Ontario and Quebec, it could be ugly due to greater manufacturing activities.

{kind=link}

Ultimately, how this all plays out is anyone’s guess. Humility is important when looking to the future. But all of the ingredients for a rather deep recession are on the table. A silver lining: Stephen Harper will have to wear it. That would, if they are paying attention, increase the odds of a federal election this Fall.